If your situation is more complex and you’re seeking personalised support, our AFSL-licensed partners at PlanningIQ offer a one-hour discovery meeting with a real financial adviser.

You’ll receive a written summary of the strategies discussed and can decide whether to proceed with further advice.

Climbing the Property Ladder – What it Takes in Real Dollars

Quick Look

Focus: How a negatively geared investment can help build long-term property wealth

Key Takeaways:

Starting with a high-debt property requires cash sacrifice in the early years

Tax benefits soften the blow, but growth and time are the real rewards

Leveraging equity into additional property can build more wealth over the longer term

Reading Time: ≈ 8 minutes

Introduction

Buying your first investment property can feel like a stretch — especially when it costs $750,000 and you’re needing $150,000 cash to meet the typical 20% deposit required by lenders. But with careful planning, many Australians use this as a stepping stone to build long-term wealth.

In this article, we walk through a realistic path up the property ladder, using real numbers over 20 years. We show how “gearing” plays a continuing role and is aided by significant tax benefits. Gearing is the term used to describe using a smaller sum to borrow a much larger sum to own a much larger asset. This has a multiplier effect such that the growth on a larger asset is more than that on a smaller asset. Hence the term “geared up”.

Furthermore, the repayments on the geared-up borrowings and the property ownership costs such as rates, insurance and repairs, usually add up to cost more than rental income that results in a negative return. Hence the term negative gearing.

Context & Problem

Many investors underestimate how much negative gearing actually costs in real money. The tax offset helps, but the cash shortfall can be significant. Understanding this is crucial before making your first move.

For our first example, we start with a $750,000 investment, 20% cash deposit with an 80% loan, and 30-year P&I at 6.5% interest. In NSW, Govt purchase duty is close to $28,000. Outgoings and rent are typical, and depreciation is factored in.

Depreciation is an accounting concept that allows a non-cash tax deduction to be claimed against taxable income for the decline in value under tax law. It usually only applies to new properties or ones less than approximately 10 – 20 years old. Although this is a tax deduction it doesn’t cost anything because it is part of the purchase price of the property.

From there, we look at what happens when the property grows at 6% p.a. and is used to fund a second investment.

Strategy & How To

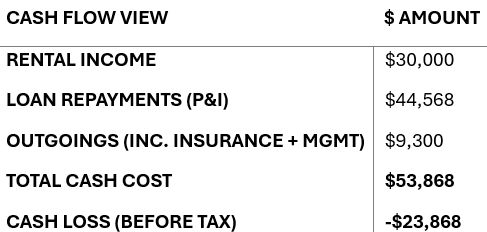

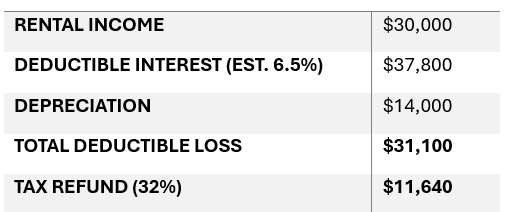

Year 1 Negative Gearing Breakdown Property Value: $750,000 Loan: $600,000 P&I at 6.5% (30 years) Rental Income: $30,000

Net Cash Loss (after tax) | -$12,228

This is roughly $235/week out of pocket in the early years. The interest portion of the P&I repayment is roughly 85% in Year 1.

Interest-only loan: $1,312,000 Total Property Value: ≈ $4.64 million Total Loans: $334,000 + $1,312,000 = $1.65 million Equity: ≈ $3.0 million

Target of $3 million equity is achieved slightly ahead of schedule due to compounding growth. Warning: these outcomes are based on the assumptions shown a which may not eventuate. This exercise may even result in an overall loss as the future cannot be predicted.

Common Questions & Misconceptions

Isn’t this too risky with high debt?

Yes, it can be — especially if interest rates rise or if you can’t cover negative cash flow. That’s why understanding the real cash cost upfront is crucial.

What if property growth is lower than 6%?

Then it will take longer to reach your equity goals. Growth is never guaranteed.

Can I afford a second property if I’m still negatively geared?

It depends on your income, borrowing capacity, and how much equity you’ve built. Banks will factor in rental income, but not the full tax benefit.

Do I need to go interest-only for the second loan?

Many investors do this to reduce cash flow pressure, especially when the first property is still being paid down.

Conclusion

Buying one investment property doesn’t make you wealthy — but managing it well and using its growth to buy another can. The journey requires patience, cash discipline, and realistic expectations about returns and risks.

After 20 years, it’s possible to hold $4.8 million in property with over $3 million in equity. But the early years will test your budget and resolve. The key is planning with real numbers, not wishful thinking.

Ready for Personalised Property Investment Advice?

Personalised recommendations based on your own figures

Easy to read digital Statements of Advice

Unlimited access to qualified Money Coaches for follow up questions

Start your moneyGPS journey now and make every super dollar work harder.

Need Full Scope Financial Planning? If you think you might need a holistic roadmap that leaves nothing out, consider booking a discovery meeting with a fully licensed Financial Planner.

Work one on one with the Planner

Get ongoing support through every stage of your financial journey.

Book a discovery call with Planning IQ today and take the first confident step towards comprehensive wealth management.

Disclosure: General information only. Consider your objectives, financial situation and needs, and seek professional advice before acting.

How We Keep It Trustworthy

Every article includes a Review & Fact Check section below — so you know exactly where our facts come from, what’s uncertain, and whether there’s any bias.

Review & Fact Check

Fact References

Loan repayments and amortisation estimates verified via Moneysmart calculators and typical bank terms

Rental income increases based on 3% CPI assumption

Property growth of 6% is hypothetical but aligns with historical long-run averages (CoreLogic data)

Tax assumptions based on 30% marginal tax rate (stated as 32% to include Medicare levy) ATO (2024–25)

Unverified or Inconclusive Items

Future growth and rent escalation rates not guaranteed

Depreciation estimates are for illustration — actual values depend on the property and tax schedule

Time Sensitivity

Loan rates and tax rules current as at June 2025

Assumptions may not reflect future interest rate or lending policy changes

Bias Assessment

Article is neutral, educational and non-promotional

Encourages readers to seek advice before acting

Start with clarity. Continue at your pace.

There’s no right or wrong next step only the one that feels right for you.

Disclaimer: All information on Super Advice Ai is general in nature only and does not take into account your personal objectives, financial situation or needs. You should consider whether any information on Super Advice Ai is appropriate to you before acting on it. If Super Advice Ai refers to a financial product, you should obtain the relevant Product Disclosure Statement (PDS) or seek professional advice from a licensed financial planner.